ONE APPChoose Alipay

Best for a short independent trip when you want one English-friendly place for payments, transport and travel services.

BEST COVERAGESet up both

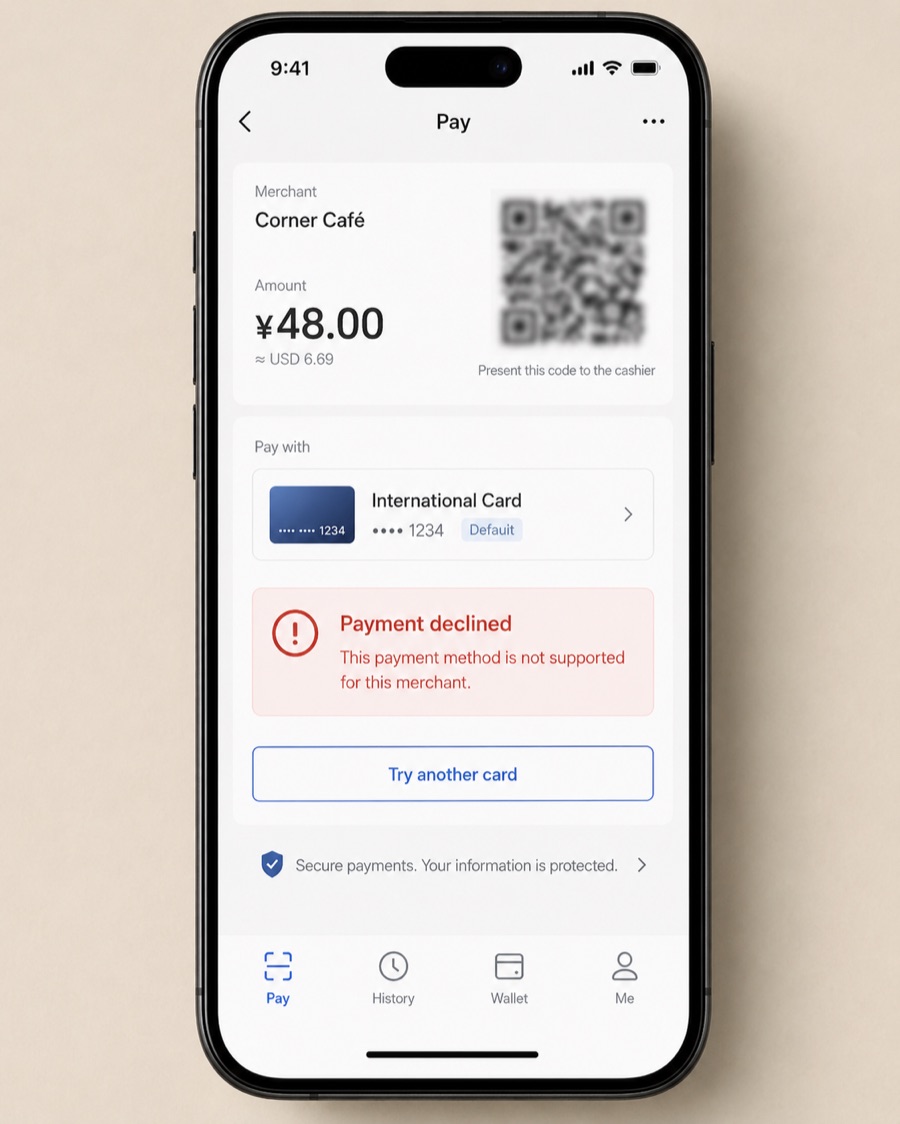

Use Alipay as primary and WeChat Pay as backup. A rejected card or unsupported merchant flow does not then end the transaction.

NON-NEGOTIABLEKeep an offline fallback

Bring a physical card from a second bank and small RMB notes. Two apps linked to one blocked card are still one payment method.

## The comparison that matters on a real trip

Both wallets can handle ordinary merchant payments in mainland China with eligible overseas cards. Both can fail. The difference shows up in what surrounds the payment.

| Question | Alipay | WeChat Pay |

|---|---|---|

| Best role for a first-time visitor | Primary travel wallet | Second wallet plus messaging layer |

| Overseas phone number | Supported | Supported |

| Passport / identity checks | May be required as the account is used | May be required; extra security review can appear |

| International cards | Major overseas card networks are supported, subject to issuer and product rules | Major overseas card networks are supported, subject to issuer and product rules |

| Tourist utilities | Strong: transport, DiDi, translation and travel mini apps | Useful, but the interface is built around chat and mini programs |

| Social contacts | Not the reason to install it | Strong: locals, guides and businesses commonly use WeChat |

| Foreign-card transfers and red packets | Do not rely on them | Do not rely on them |

| Which merchants accept it | Very broad | Very broad |

| Guaranteed to work everywhere | No | No |

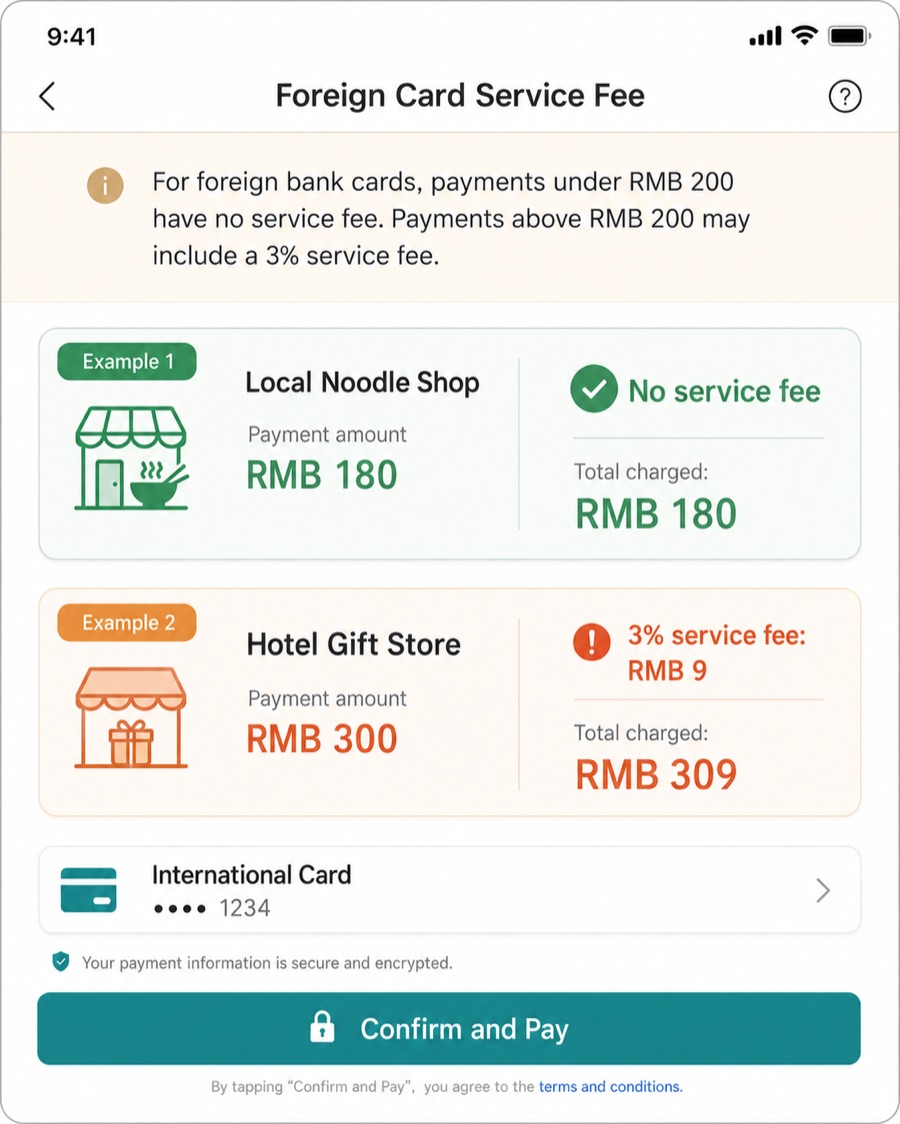

The official 2025 guide for international visitors says foreigners can register mobile-payment apps with a foreign or Chinese phone number and bind cards from major networks. It also warns that card brands, charging standards and limits can vary by product; the screen in front of you is the final rule. See the [Chinese government’s guide to working and living in China](https://english.www.gov.cn/2025special/bizexpatsinchina2025).

## Why Alipay is usually the better first install

Alipay feels closer to a visitor control panel. The home screen is busy, but the useful pieces are recognizable: Pay, Scan, Transport, DiDi, translation and travel services. The app supports multiple languages, and China has explicitly promoted its travel functions for overseas visitors.

That makes Alipay the simpler answer for someone who wants to:

- Pay at a convenience store five minutes after landing.

- Open a city transport code.

- Call a DiDi without creating another payment setup.

- Use in-app translation around a Chinese mini program.

- Keep tickets, rides and everyday payments in one place.

It is still worth reading our separate [Alipay setup and card-decline guide](/en/pay/alipay-for-foreigners/). This comparison page tells you which wallet to try; that guide deals with passport verification, personal QR codes and a card that appears linked but refuses to pay.

## Why WeChat Pay is worth the second setup

WeChat Pay sits inside an app you may need anyway. Hotels, guides, restaurant hosts and people you meet are more likely to exchange a WeChat contact than an email address. Restaurant ordering, attraction notices, queue systems and customer service often live in WeChat mini programs.

This does not mean WeChat Pay is universally better at small vendors. It means it gives you another route when:

- A merchant shows a WeChat code first.

- Your card works in WeChat Pay but not in the Alipay checkout you opened.

- A booking or restaurant flow already lives inside WeChat.

- A local contact sends the correct merchant or mini-program page in chat.

Community reports often say that WeChat asked for an extra verification step, sometimes involving more identity proof. Treat that as a possible security review, not a fixed rule that every foreign user needs a Chinese friend. If WeChat activates cleanly, keep it. If registration becomes a time sink the night before departure, finish Alipay and preserve a physical backup instead.

## The setup order that creates real redundancy

CONVENIENCE STOREAlipay first

Open your payment code and let the cashier scan it. WeChat Pay and cash are immediate backups.

STREET STALLUse the merchant’s supported rail

Try the displayed wallet, but keep small cash ready if the code is personal or foreign cards are not enabled.

DIDI / TAXIAlipay is convenient

Booking and payment can stay inside one app. For a street taxi, agree on the payment method before the ride ends.

RESTAURANT MINI PROGRAMWeChat may fit the flow

Ordering and queues often live in WeChat. If the mini-program checkout rejects the card, ask for the cashier’s normal merchant code.

METROUse the city-specific transport route

Alipay often exposes it clearly. A ticket machine or staffed counter is safer than debugging a transport code before a train.

HOTEL / LARGE PURCHASECompare with a physical card

Ask whether the desk accepts your card network directly. The 3% wallet fee can matter on a large bill.

## The QR code is often the real difference

At the counter, “pay by QR” can describe several different transactions:

- You show a payment code and the cashier scans it.

- You scan a registered merchant code and enter the amount.

- You scan a personal collection code that behaves more like a transfer.

- A mini program creates an in-app order with its own card-acceptance rules.

Foreign cards are designed mainly for consumption at supported merchants. They do not turn either account into a full local wallet. Red packets, person-to-person transfers, balance top-ups and some personal collection codes may be unavailable.

When a sticker code fails, ask: “Business QR code?” or show this Chinese sentence:

> 可以用商家收款码或者扫码枪吗?

> *Kěyǐ yòng shāngjiā shōukuǎn mǎ huòzhě sǎomǎ qiāng ma?*

> Can I use the merchant QR code or cashier scanner?

Trying the other wallet can work because the merchant enabled one route but not the other. It cannot fix a transaction that is fundamentally a transfer rather than a supported merchant payment.

## If one wallet fails and the other works, that is normal