Payments

Alipay for Foreigners in China (2026): Setup, 3% Fees, QR Traps & Card Declines

How foreign visitors can use Alipay in China with an overseas Visa or Mastercard, what the 200 RMB fee rule means, why foreign cards still fail, and how to handle personal QR codes, limits and declined payments.

The annoying Alipay problem is rarely “I cannot install the app.” It is this: you are standing at a counter in China, your Visa or Mastercard is already sitting inside Alipay, the cashier is waiting, and the payment still fails.

That is why this guide starts after the obvious setup advice. Yes, you should install Alipay, verify your passport, and add a card before you fly. But the part that saves a trip is knowing which QR codes work, why a foreign card can be visible but unusable, and when to stop retrying before the app or your bank gets suspicious.

What changed for foreign visitors

For years, short-term visitors got squeezed from both sides: China was already cash-light, but many mobile-payment flows still assumed a Chinese ID or a Chinese bank card. That gap has narrowed. Foreign visitors can now use Alipay with overseas-issued bank cards for many everyday QR-code payments in mainland China.

The practical reality is much better than it was a few years ago. It is not magic. Official policy has pushed payment platforms, banks, airports, hotels, scenic spots, and transport hubs to improve payment access for overseas visitors. In 2024, Chinese authorities also raised mobile-payment caps for foreign visitors: the single-transaction limit was raised to about US$5,000, and the annual cumulative limit to about US$50,000.

Most tourist payments are nowhere near those caps. The failures usually come from a more ordinary place:

| Problem | What it looks like |

|---|---|

| Merchant type | A personal QR code, transfer request, or unsupported mini program will not accept a foreign card. |

| Bank risk control | Your home bank blocks the first China-platform transaction. |

| Alipay risk control | The app asks for more card/passport proof after several successful payments. |

| Identity mismatch | Passport name, cardholder name, phone region, or document type does not line up. |

| Amount/fee confusion | A payment over RMB 200 adds a 3% service fee, or a larger purchase hits a limit. |

Setup checklist before you fly

Do this on stable Wi-Fi before departure. Airport Wi-Fi, jet lag, passport glare, and a bank fraud alert are a bad combination.

- Download the mainland Alipay app from the App Store or Google Play.

- Register with your own phone number. A Chinese number is not required for normal tourist use, but your number must receive SMS or calls.

- Set your document type to passport. Do not choose a mainland Chinese ID option by mistake.

- Add a supported overseas card. Visa and Mastercard are the safest choices. Some other networks may work, but do not make a less common card your only plan.

- Complete real-name verification. Use a clear passport photo page, no glare, and the same name order as your passport.

- Keep your banking app ready. Your bank may ask you to approve a suspicious foreign or online transaction.

- Install data before arrival. You need mobile data for Alipay, bank alerts, maps, ride-hailing, and support chat. See our China eSIM guide.

The first payment test

After landing, resist the urge to treat a linked card as proof that everything works. Test Alipay with a small purchase while you are still somewhere forgiving: the airport, a train station, a hotel lobby, or a convenience store.

Use this order:

- Open Alipay and make sure you are still logged in.

- Buy water or coffee under RMB 20.

- Let the cashier scan your Alipay payment code.

- If that works, scan a merchant QR code yourself.

- Check whether your home bank sends a fraud alert.

If the first small payment works, good. You have cleared the hurdle that catches many visitors. If it fails, fix it there, while you still have Wi-Fi, staff, lighting, and time.

Paying by QR code: show code vs scan code

This is where many foreign-card guides get too neat. “Pay by QR code” sounds like one thing, but at the counter it can mean two different flows:

| Method | How it works | Foreign-card reliability |

|---|---|---|

| Merchant scans you | You open Alipay’s payment code and the cashier scans it. | Usually the most reliable. Try this first. |

| You scan merchant QR | You scan a QR sticker or checkout screen, enter amount, and pay. | Usually works for registered merchants, but can fail on personal QR codes. |

If one method fails, try the other before giving up. A very common pattern is: scanning a small vendor’s QR code fails, but the payment goes through when a proper cashier terminal scans the visitor’s Alipay code.

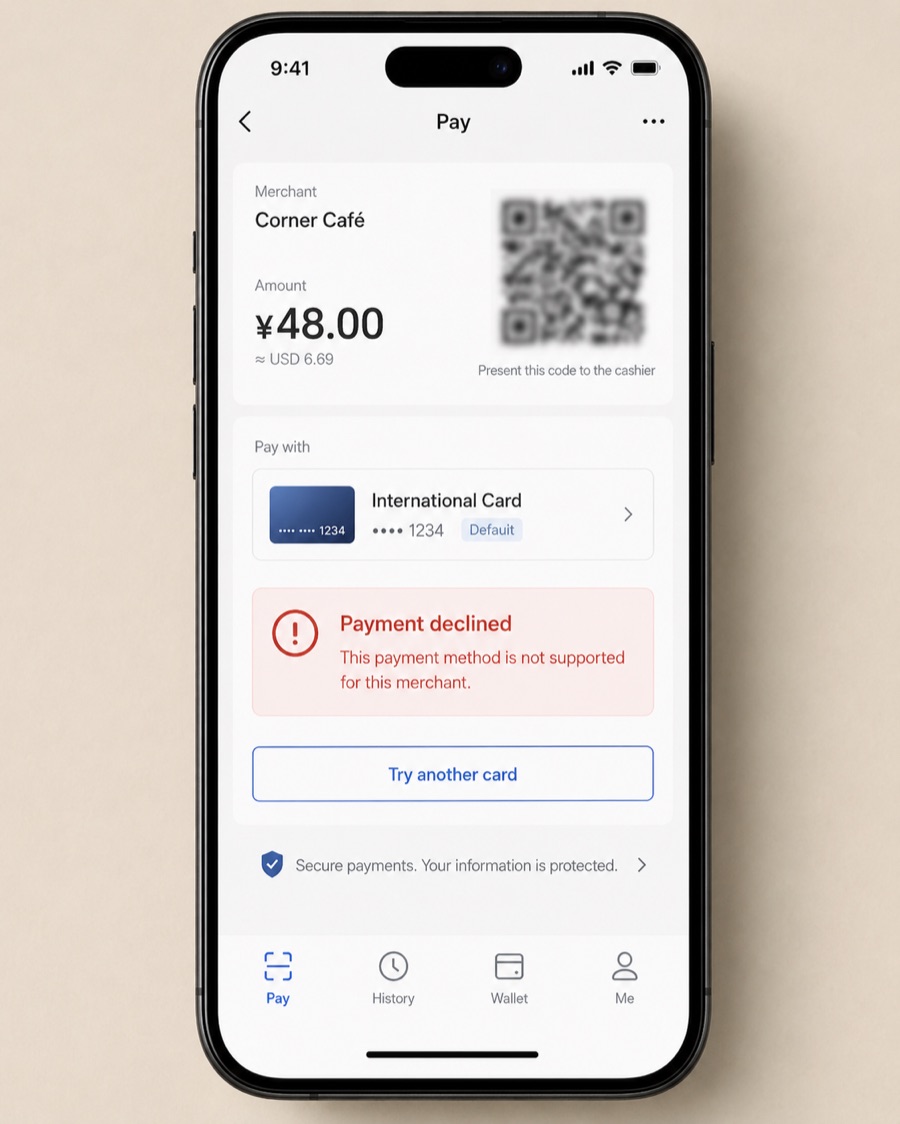

The personal QR trap

This is the Alipay problem that looks silly until it happens to you.

With a foreign card linked to Alipay, you can normally pay merchants. You usually cannot use that card for ordinary person-to-person transfers. A tiny restaurant, market stall, guide, driver, or street vendor may show a personal QR code instead of a business merchant code. To you, both are squares on a phone. To Alipay, one may be a merchant payment and the other may be a transfer.

If Alipay says the payment method is not supported:

| Try this | Why |

|---|---|

| Ask if they have a business QR code or cashier scanner. | Foreign cards are more likely to work on merchant accounts. |

| Switch to WeChat Pay if you set it up. | Some vendors are more used to WeChat Pay. |

| Pay cash for small amounts. | RMB 50-200 in small notes solves many street-level failures. |

| Ask your hotel/front desk for help with a local app order. | Useful for tickets, food delivery, or ride-hailing edge cases. |

If the same personal QR code fails a few times, stop. More taps rarely solve this problem, and repeated failed attempts can make a risk-control problem worse.

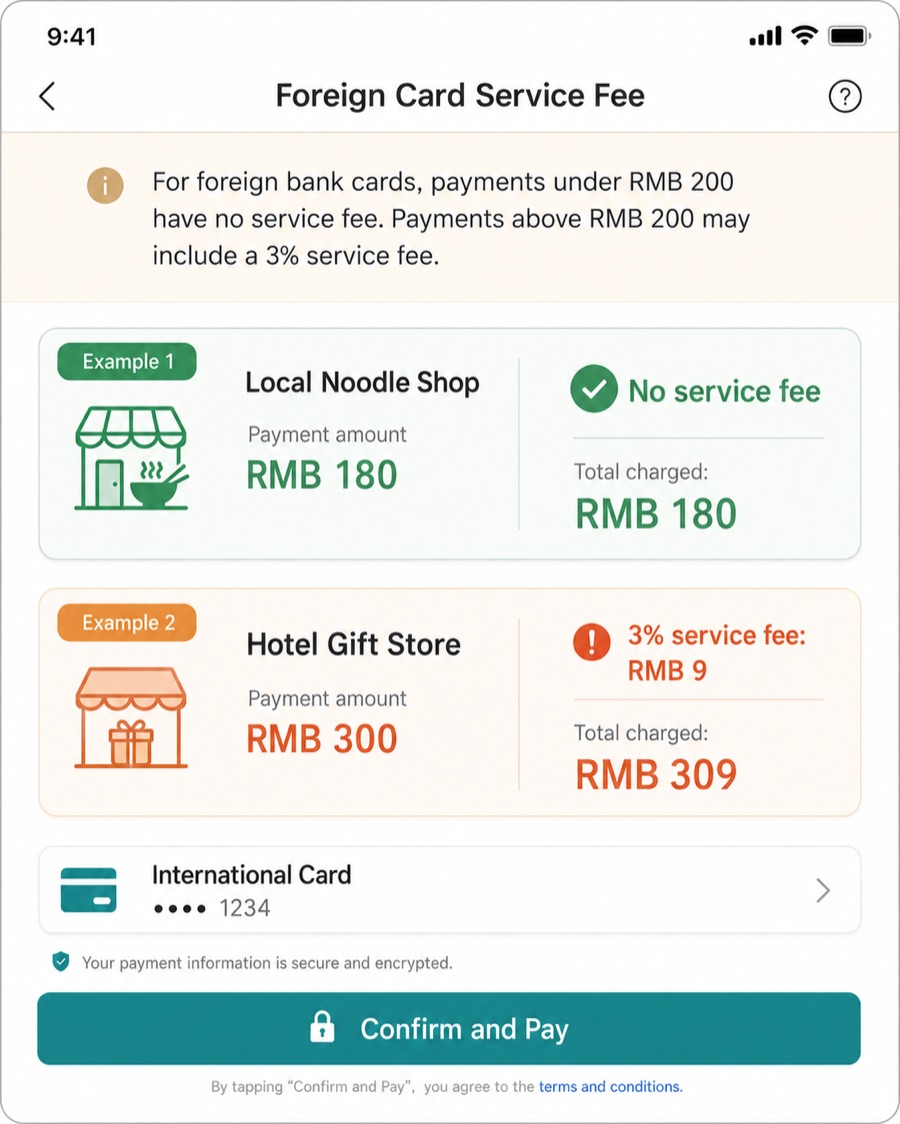

Fees: the RMB 200 rule

For overseas bank cards linked inside Alipay, remember the RMB 200 line:

| Payment amount | Service fee |

|---|---|

| RMB 200 or below | Usually no service fee |

| Over RMB 200 | Usually 3% service fee |

The fee is applied to the transaction, not to your whole trip. A RMB 180 meal is usually fee-free. A RMB 300 bill may add RMB 9. If you refund a payment, the service fee should generally be refunded proportionally.

Some travelers try to split a bill into smaller payments. It can work if the merchant agrees and the situation is casual. I would not build a hotel checkout, attraction ticket, or busy restaurant plan around it. For a large purchase, compare:

- Alipay with foreign card plus 3%.

- A physical Visa/Mastercard at a hotel or large retailer.

- A UnionPay card if you have one.

- Cash only when the amount is reasonable and you can get a receipt.

Limits: what the higher cap really means

China has raised mobile-payment limits for foreign visitors, so normal tourism spending should not hit the official ceiling. The headline cap is now about US$5,000 per transaction and about US$50,000 per year for overseas visitors using major mobile payment apps.

That does not make every RMB 1,000 payment easy. Three different limits can still block you:

| Limit source | Example |

|---|---|

| Official platform cap | Very large purchases or cumulative annual spend. |

| Your home bank | Card-not-present, foreign, or high-risk transaction limits. |

| Merchant/app rule | A ticketing, delivery, hotel, or personal QR flow may not accept foreign cards. |

If a RMB 1,000-2,000 payment fails even though you are far below the official cap, do not spend ten minutes thinking about national policy. Look first at your bank, the merchant flow, and Alipay risk control.

What Alipay with a foreign card cannot do

This is the mental model that prevents a lot of frustration: a card showing inside Alipay does not turn your account into a full local Chinese wallet.

Foreign-card Alipay is mainly for consumption payments. Do not expect it to reliably support:

- Person-to-person transfers.

- Red packets.

- Balance top-ups.

- Huabei or other credit/finance features.

- Wealth management or insurance products.

- Some China-only mini programs.

- Paying a friend’s personal collection code in every case.

For restaurants, coffee shops, metro codes, ride-hailing, convenience stores, and many tourist-facing merchants, Alipay is still worth setting up. For living like a local account, expect walls.

Card declined: fix it in this order

At the counter, the worst move is to panic-delete cards and add them again. Work from the outside in: merchant flow, bank approval, identity, then Alipay risk control.

| Symptom | Most likely cause | What to do |

|---|---|---|

| ”Only mainland China cards supported” | You are in a transfer/top-up/unsupported flow, not normal merchant payment. | Go back to payment code or merchant QR. Avoid transfer and balance top-up flows. |

| ”This payment method is not supported” | Personal QR, mini program, or merchant category does not accept foreign cards. | Ask for a business QR/cashier scanner; try WeChat Pay or cash. |

| Card added but every payment fails | Your bank blocked the transaction or requires 3-D Secure approval. | Open your banking app, approve the alert, or call the bank. Tell them you are using Alipay in China. |

| Passport verification fails | Glare, wrong document type, name mismatch, or unclear photo. | Use soft light, dark matte background, passport as document type, and exact passport name. |

| Payment worked before, now blocked | Alipay risk control or unusual transaction pattern. | Stop repeated attempts; contact Alipay support and prepare card/passport proof if requested. |

| You need to pay a large amount | Platform, bank, or merchant limit. | Try a physical card at a major counter, split only if reasonable, or ask the merchant for supported options. |

The 60-second failure tree

When a payment fails and someone is waiting behind you, use this order:

-

Is this a personal QR code?

If yes, ask for a business QR code or cashier scanner. If they only have a personal code, switch to WeChat Pay or cash. -

Did the merchant scan your code, or did you scan theirs?

If you scanned theirs and it failed, open your Alipay payment code and ask the cashier to scan you. -

Did your bank send an alert?

Open your banking app immediately. Many declines are not Alipay failures; they are your bank waiting for fraud approval. -

Is the amount over RMB 200 or unusually large?

Expect the 3% fee and possible bank review. For hotels, expensive tickets, or shopping, ask whether a physical card counter is available. -

Have you failed three times in a row?

Stop retrying. Switch payment method first. Repeated attempts can look suspicious and trigger more risk checks.

Name and passport details matter

Identity mismatch is boring, but it breaks payments.

Before blaming Alipay, check:

- Is your document type passport, not mainland ID?

- Does your name match the passport and card? Watch middle names, hyphens, spaces, and accents.

- Did you enter the passport number exactly?

- Is the card active for online and overseas transactions?

- Does the card have enough available balance or credit for a small verification hold?

If your card has no printed name, is virtual-only, or uses a different billing name, keep another card ready. Some risk-control reviews may ask for card proof that virtual cards cannot provide cleanly.

Alipay vs WeChat Pay

For most visitors, Alipay is the app I would set up first. WeChat Pay is the backup that prevents one bad QR code from becoming your whole afternoon.

| Question | Alipay | WeChat Pay |

|---|---|---|

| Best use | Tourist payments, transport, services, many mini programs | Messaging, social contacts, merchants who prefer WeChat |

| Setup difficulty | Usually easier for foreigners | Can be more sensitive to account verification |

| Foreign card use | Good for merchant payments | Good as a backup where accepted |

| Must-have? | Yes, if you want one primary app | Strongly recommended if you can set it up |

WeChat Pay is not automatically better. It is the second rail. Some vendors only show WeChat, some only show Alipay, and many accept both.

Do you need a Chinese phone number?

For ordinary Alipay setup, no. You can register with an overseas number. The fragile part is not the Chinese number; it is being in China with no reliable data when your bank or Alipay wants to verify you.

You may need phone access for:

- Bank SMS or app approval.

- Alipay login and security checks.

- Ride-hailing driver calls.

- Hotel or ticketing mini programs.

- Receiving one-time codes from your home bank.

A roaming plan or travel eSIM is often enough for tourists. A local Chinese SIM can help with local apps, but it is not required just to make Alipay merchant payments.

Backup plan if Alipay fails

Do not make Alipay your only payment method on day one. The goal is not to carry five wallets forever. It is to get through the first 24 hours without one failed QR code controlling the day.

| Backup | Why it matters |

|---|---|

| WeChat Pay | Useful when a merchant prefers WeChat or Alipay is blocked. |

| Second Visa/Mastercard | One bank may block what another approves. |

| RMB cash in small notes | Solves taxis, small vendors, and urgent low-value purchases. |

| Physical card | Still useful at hotels, big malls, airline counters, and international chains. |

| Hotel front desk | Can help with addresses, taxis, local calls, or app-only bookings. |

For cash, avoid carrying only RMB 100 notes. If a vendor has no change, your money is technically valid and practically useless.

Which payment method to try by scene

| Scene | Try first | Backup |

|---|---|---|

| Airport coffee / convenience store | Alipay payment code | WeChat Pay or cash |

| Street food / small stall | Alipay merchant scan if available | Cash in small notes |

| Taxi or DiDi | Alipay inside the app | WeChat Pay, cash taxi, hotel help |

| Metro | Alipay transport QR after setup | Ticket machine, service counter, cash/card where available |

| Hotel | Physical card or Alipay | Ask front desk which card network works |

| Scenic-area tickets | Official app/site or Trip.com-style platform | On-site counter, hotel/concierge help |

| Personal guide / small driver | Agree method before service | Cash, WeChat Pay, or a proper merchant QR |

A good first-day payment sequence

If I were landing in China with a foreign card today, this is the order I would use:

- Turn on your eSIM or roaming.

- Open Alipay and confirm login.

- Buy one small item under RMB 20.

- Add WeChat Pay if your account allows it.

- Withdraw or exchange a small amount of RMB cash in mixed notes.

- Save your hotel’s Chinese name, address, and phone number.

- Use Alipay or WeChat inside DiDi or transport apps only after the first small payment works.

This is not glamorous travel advice. It is the boring sequence that keeps a card that “should work” from ruining your first evening.

Outdated or risky advice to ignore

| Advice you may still see | What to do instead |

|---|---|

| ”Use Tour Pass first.” | For normal tourists, direct overseas-card binding is now the main path. |

| ”If Alipay fails, keep trying.” | Stop after a few failures and switch method; repeated retries can worsen risk control. |

| ”Ask a friend to transfer RMB into your account.” | Do not rely on transfers as a tourist; foreign-card accounts have wallet restrictions. |

| ”Any QR code is fine.” | Personal QR codes and merchant QR codes are not the same for foreign cards. |

| ”Cash solves everything.” | Cash helps, but China is QR-first and vendors may not have change. |

Common questions

Can I use Alipay without a Chinese bank account?

Yes, for merchant payments. You can register with an overseas phone number, verify with a passport, and link an overseas bank card. But you should not expect full local-wallet functions such as transfers or red packets.

Can I receive money from a Chinese friend into Alipay?

Do not rely on this as a tourist. Foreign-card accounts are not the same as local balance wallets, and person-to-person transfers are exactly where many restrictions appear.

Can I pay a personal QR code?

Sometimes no. A personal collection code may be treated like a transfer, and foreign cards often cannot be used for that. Ask for a merchant QR, cashier scanner, WeChat Pay, or pay cash.

Does the 3% fee apply if my card has no foreign transaction fee?

Yes, these are different fees. A no-foreign-transaction-fee card may save your bank’s fee, but Alipay’s foreign-card service fee can still apply above RMB 200.

Is Tour Pass still needed?

No for most visitors. Older guides mention Alipay Tour Pass or TourCard-style prepaid products. For a normal 2026 tourist trip, direct card linking is the main path. If a guide tells you to top up a prepaid Alipay wallet first, check the date.

Can I use Alipay for metro rides?

Often yes, but metro QR setup varies by city and may require its own transport card flow inside Alipay. Test a small ordinary store payment before relying on metro QR codes.

What should I do if Alipay support asks for card proof?

Use the in-app support flow. Be ready to show that the card belongs to you. If your card is virtual-only or has no printed name, use a second physical card as backup.